Bank Strategy Briefing: Bank acquisitions by credit unions

Bank Strategy Briefing: Bank acquisitions by credit unions

Authored By

Peter Wilder

Practices

A new trend is developing in the bank versus credit union debate. Credit unions are aggressively pursuing bank acquisitions – winning over sellers with large cash premiums and frustrating other community bank buyers that cannot bid competitively.

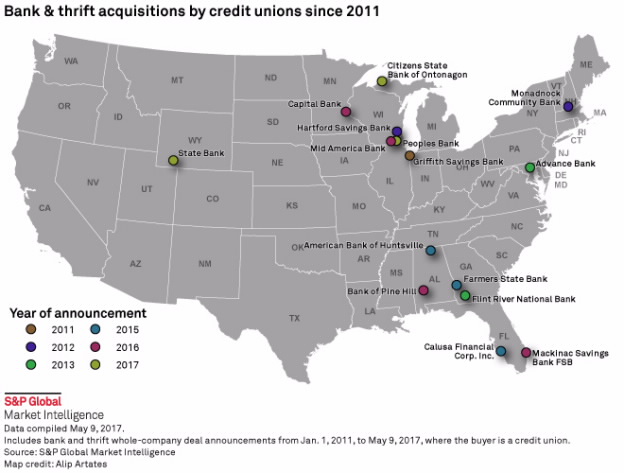

The Trend1

Below is a map showing bank acquisitions by credit unions since 2011. During that period, there have been 15 acquisitions of community banks by credit unions nationally. Six have occurred in the Upper Midwest, with four involving a Wisconsin institution as buyer or seller. (That’s more than any other state in the country.)

Credit unions are cash buyers, and they have two big advantages over most acquisitive banks. First, credit unions have no shareholders, so they can easily “overpay” without fear of shareholder retribution. Second, given that a selling bank’s future income stream will be tax free for an acquiring credit union, they can offer a far higher premium than a bank suitor.

What Does This Mean?

On one hand, banks wishing to cash out have a potential group of acquirers who can offer inflated premiums driven by their unique tax advantage, which is ultimately good for shareholders. On the other hand, as this trend continues many banks wishing to grow by acquisition will miss out on acquisition opportunities that just a few years ago would have been within their grasp. The income tax savings enjoyed by acquisitive credit unions may be an insurmountable hurdle for traditional bank bidders.

Possible Strategies

If the banking industry determines that these bank acquisitions by credit unions are, on the whole, a net negative, one solution is to advocate for an “acquisition tax” to be paid by credit unions at the state and/or federal level at the time of acquisition. Such a tax could help level the playing field for acquisitive banks and also protect taxpayers (at least in part) from the loss of tax revenue on income generated by a bank one day and by a credit union the next.

Another strategy is for community banks—either individually or with one or more other community banks—to explore the possibility of acquiring a credit union. Such a transaction would eliminate a credit union competitor and would also give credit union members a lump sum payment that could exceed the savings they might expect on more favorable interest rates and fees. Challenges abound with this strategy, including finding a credit union with a balance sheet that is palatable enough to acquire, navigating a very complex structuring and regulatory approval process, and retaining the credit union’s members as customers.

Whatever your bank’s situation, know that credit unions (and their lawyers and investment bankers) are actively and aggressively searching for banks to acquire, adding a new and rapidly expanding dimension to credit union competition.

1Source: S&P Global Market Intelligence LLC. Contains copyrighted and trade secret material distributed under license from SNL. For recipient’s internal use only.

Authored By