Bank Strategy Briefing: Bank Consolidation - Digging a Bit Deeper

Bank Strategy Briefing: Bank Consolidation - Digging a Bit Deeper

Authored By

Peter Wilder

Practices

Consolidation in the industry is one of the most frequently discussed topics among banking circles. However, other than the fact that the number of charters continues to decline, it is sometimes difficult to pinpoint meaningful trends in the data cited in articles and at seminars. This is due to the fact that most data reflects national rather than local data, and the data often focuses on the number of charters rather than the relative pace of consolidation.

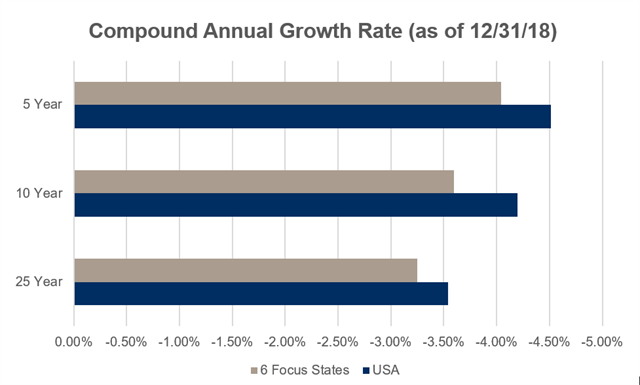

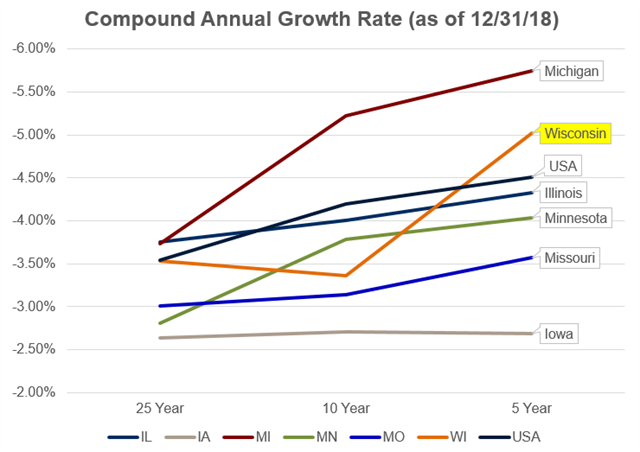

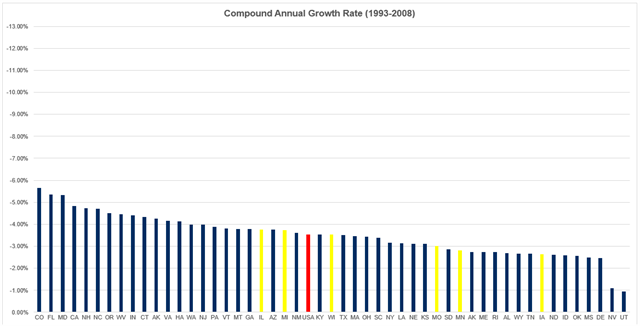

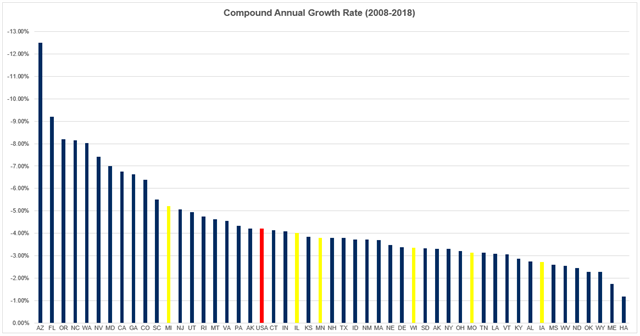

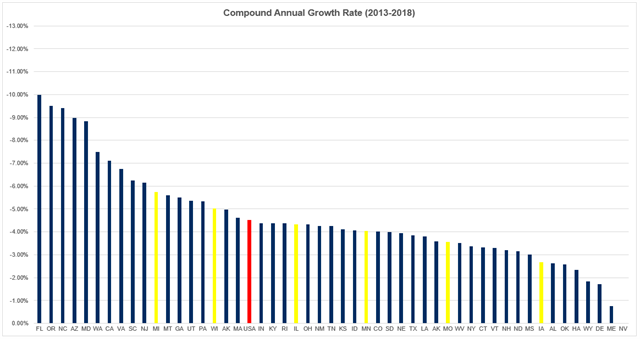

We looked into the relative pace of consolidation, historically, at the national and state levels for FDIC-insured institutions based on compound annual growth rates (CAGR)—which, since we have a shrinking number of charters, can more aptly be thought of as a compound annual consolidation rate—over the past 25 years, 10 years and 5 years ending Dec. 31, 2018. Graphs reflecting the data appear at the end of this edition of Bank Strategy Briefing, and we have highlighted the national average as well as rates for the six Midwestern "focus states" that we regularly follow (Wisconsin, Missouri, Minnesota, Michigan, Iowa and Illinois). Here are some interesting trends:

-

More Banks ≠ More Consolidation. Over the last 25 years, our focus states have accounted for roughly 27-29% of all banks in the United States, and many industry spectators consider the Midwest in general to be "over banked." You would think this would drive an above-average rate of consolidation when compared to national averages, but, in fact, the opposite is true. The rate of consolidation for these six states as a group has actually been slower than the national average. This is likely due to several complex factors, which we believe may include the relatively low bank failure rate in the Midwest and an especially strong culture of independent community banking, among others.

-

Something is Happening in Wisconsin. Our home state of Wisconsin has experienced a relatively average rate of consolidation over 25- and 10-year time horizons. However, over the last 5 years, Wisconsin has seen a pronounced spike in consolidation rate that is anomalous. Based on the high volume of M&A activity to date in 2019, that trend is continuing in earnest. While we cannot point to any specific reason underlying this substantial acceleration of consolidation in Wisconsin, we think it may be explained by a combination of (i) the emergence of multiple serial acquirers, (ii) an increased interest in Wisconsin by out of state acquirers, and (iii) a heightened focus by M&A advisors in the state in recent years.

-

Michigan and Iowa are Bookends. As illustrated by the graph above, Michigan and Iowa reflect opposite ends of the consolidation spectrum. These "goalposts"—likely the result of differing economic, legislative and cultural histories—show how variable consolidation trends can be even among states in similar geographic regions.

Our attorneys regularly share our observations on trends in the banking industry with peer groups, boards and management teams. If you are interested in a guest speaker, please contact us.

25 Year

10 Year

5 Year

Authored By