Bank Strategy Briefing: Recession watch - Actions community bank boards can take now

Bank Strategy Briefing: Recession watch - Actions community bank boards can take now

Authored By

Peter Wilder

Practices

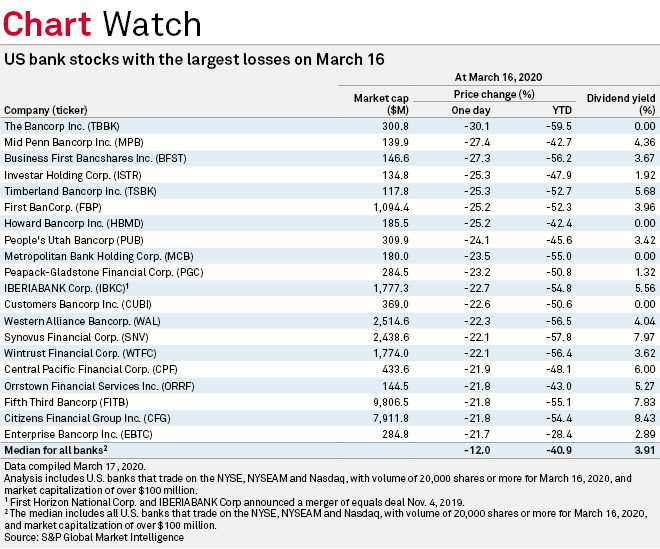

“While economic data for March is just starting to be released, the severity of the blow from the coronavirus (COVID-19) leads us to believe that the U.S. is entering recession – if not already in one.”

S&P Global Research Note

March 17, 2020

After more than a decade of recovery and expansion since the Great Recession, it appears community banks may be in for a rough patch. Although it is impossible to know just how challenging this new economic cycle will be for community banks, markets are anticipating the potential for significant credit quality issues for publicly traded banks.

Community bank boards and executive teams can look to lessons learned in the Great Recession to begin preparing now for possible hardship, rather than taking a ‘wait and see’ approach.

Eight topics for a special board meeting

Consider calling a special board meeting to address the following 8 ideas and to brainstorm your own ideas on preparing for the impacts of a likely recession:

1. Stress testing

Commence a fresh review of your loan concentrations and consider whether your team, perhaps with the help of a third party, can develop a meaningful stress test based on today’s known macroeconomic stressors.

2. Loan reviews

Consider increasing the frequency and scope of third party loan reviews to identify specific credit quality issues as early as possible.

3. Workouts and accommodations

Conduct a review of significant loan relationships to identify high and low risk borrowers. Develop a plan for which borrowers you will or will not likely be willing to work with on a workout or accommodation. Review regulatory guidelines and your loan policy regarding troubled debt restructurings (TDRs).

4. Staffing

Create a staffing plan to handle an influx of classified loans, including identifying outside parties (e.g. lawyer, property manager, etc.) who will assist with workouts and foreclosures.

5. ALM

Reassess your bank’s interest rate risk under various recessionary scenarios that now appear more likely, including a prolonged Federal Reserve zero interest rate environment. Take advantage of outside expertise and scale by engaging a third party ALM consultant.

6. Capital plan

Consider whether or when you should suspend or reduce stock buybacks and dividends. Identify sources of capital should the bank suffer material provisions or credit losses. If the bank’s correspondent line is discontinued, what other options are available? Will subordinated debt be too expensive? Do you have adequate shares authorized for a private placement of common or preferred stock? Are directors prepared to ‘pass the hat’? How would you prioritize assets for disposition if you need to shrink the bank’s balance sheet?

7. Liquidity plan

Perform a liquidity stress test and identify contingent liquidity sources, such as brokered deposits, FHLB advances and the sale of loans or securities.

8. Communications plan

Prepare a plan to communicate regularly with shareholders and customers. Reassure them of the safety of deposits and the steps being taken to address the effects of a recession on the bank.

A little perspective

As you prepare for possible challenges ahead, it’s important to remember that most banks survive even the most difficult recessions. In fact, many come out stronger on the other side.

Authored By