Bank Strategy Briefing: What happened to all that talk about noninterest income?

Bank Strategy Briefing: What happened to all that talk about noninterest income?

Authored By

Peter Wilder

Practices

In the years following the Great Recession, a focus on noninterest income became one of the common themes at community bank conferences and in industry publications. Historically low interest rates were (and still are to a lesser extent) suffocating net interest margins and income, causing many proactive bankers and industry experts to look more closely at other revenue sources that were not interest rate dependent.

Anecdotally, over the last couple of years the “shouts” calling for a focus on more noninterest income sources have turned into “whimpers,” likely due to increasing loan demand and thawing interest rates. That made us wonder: did the call-to-action on noninterest income yield any identifiable shift in strategy by banks?

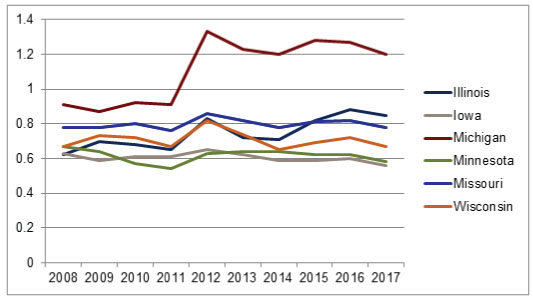

In short, it does not appear that banks’ relative mix of noninterest income has changed post-Great Recession. Rather, noninterest income as a percentage of average assets has generally remained relatively flat among banks in our region of Illinois, Iowa, Minnesota, Missouri and Wisconsin (Michigan being the exception), and the slight volatility can likely be attributed to mortgage refinance activity as mortgage rates ebbed and flowed over the last several years.

Noninterest Income / Average Assets (%)1

There are many possible explanations for why banks as a whole in our region have not achieved noninterest income growth despite the lessons learned in the most recent economic and interest rate cycle. For example, competition has held deposit account and loan fees in check. It is also possible that the hope of interest rate movements simply took longer than most banks anticipated, causing banks to ignore a focus on new noninterest income sources while expecting a quicker return to more traditional interest rates.

However, the fact remains that shareholder returns are positively correlated with noninterest income. Consider the fact that in the six states referenced above, there are 1,326 state-chartered banks with less than $5 billion in total assets. Of those banks, 534 of them achieved a 10% or better ROAE in 2017 and had an average noninterest income to assets ratio of 0.78%. The remaining 792 banks that fell short of a 10% ROAE averaged a significantly lower ratio of 0.63%.

We recommend that community bank management teams and boards include revenue stream diversification as an agenda item for a board meeting or strategic planning session. Have a trusted advisor attend to discuss what opportunities are permissible to pursue additional revenue growth. The recent economic environment has been very favorable for community banks. Now is the time to plan for enhanced shareholder returns and to set your bank up to weather the next economic downturn.

1Excluding trust company banks.

Authored By